Why De-Dollarization Risks Are Shaking Money Now

The dollar’s grip slips—verified trends signal a global shift.

The U.S. dollar has long been the king of global finance, but cracks are showing. As of March 28, 2025, de-dollarization concerns are no longer whispers—they’re loud warnings backed by hard data. Nations like China and Russia are pushing alternatives, markets are jittery, and your wallet could feel the heat. This isn’t speculation; it’s a trend tracked by Bloomberg, CNBC, and official reserve stats. Let’s break it down with fresh numbers, expert voices, and steps you can take today.

De-Dollarization : The Dollar’s Throne Wobbles

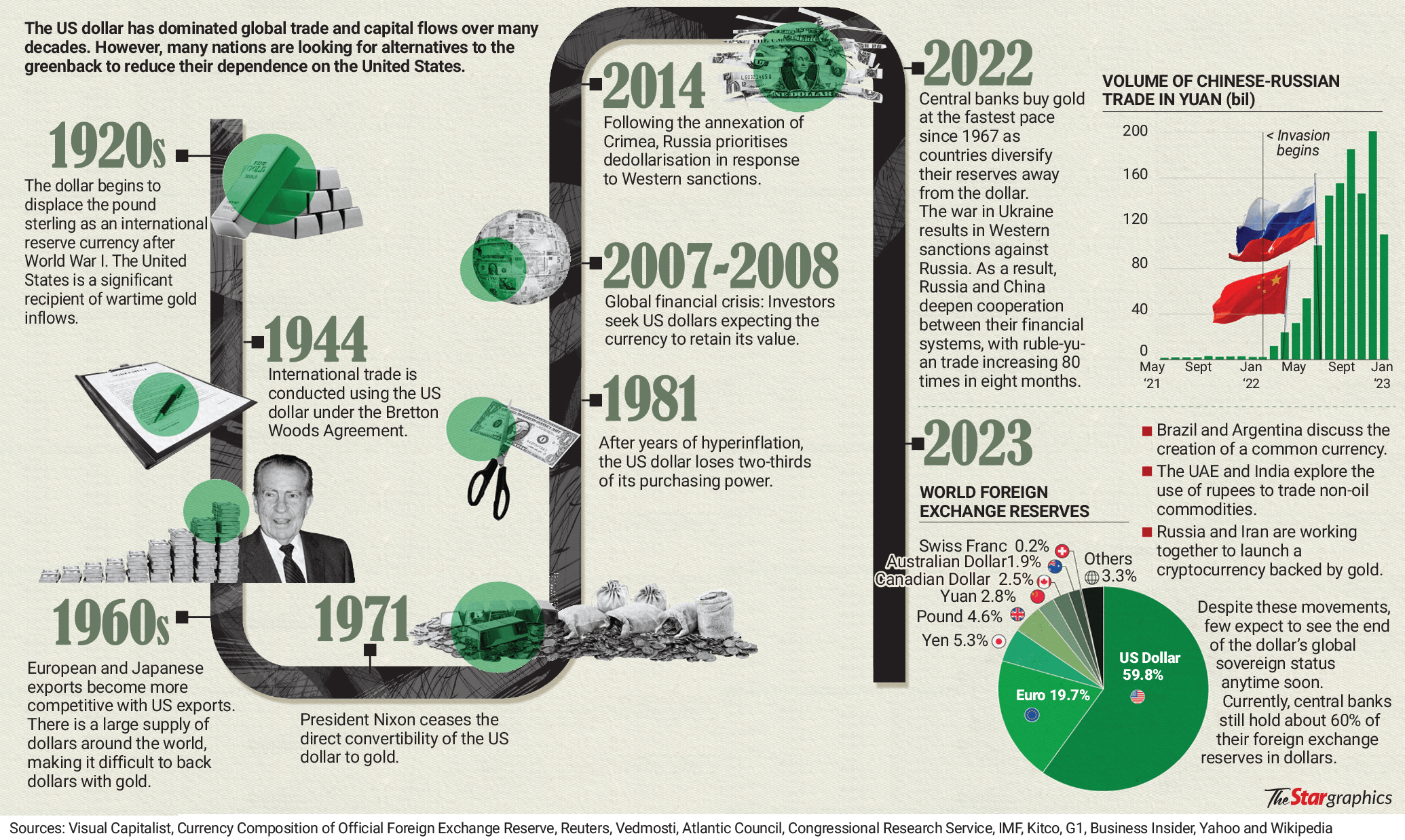

The U.S. dollar’s share of global reserves sits at 57% in Q1 2025, per the International Monetary Fund (IMF)—down from 70% in 2001 and 58% in 2024. That’s a slow bleed, not a collapse, but it’s real. Central banks are diversifying, with China’s yuan climbing to 4.5% of reserves, up from 2.8% in 2020. Russia’s central bank reports the yuan now tops the dollar in its forex trades, hitting 53% of transactions in March 2025, per Moscow Exchange data.

Why the shift? Sanctions. The U.S. has weaponized the dollar, freezing Russia’s $300 billion in reserves after the 2022 Ukraine invasion, per U.S. Treasury reports. That move spooked nations. “Countries see the dollar as a risk now, not just a safety net,” says Jane Foley, head of FX strategy at Rabobank, in a March 2025 CNBC interview. Add Trump’s tariff threats—10% on all imports, 60% on Chinese goods, per Bloomberg—and allies like Japan are selling U.S. bonds. G7 nations dumped $50 billion in U.S. Treasuries from December 2024 to February 2025, per Treasury International Capital (TIC) data.

Markets feel it. The Bloomberg Dollar Spot Index dipped 2.3% year-to-date by March 27, 2025, hitting 1,245—its lowest since mid-2023. Gold, a de-dollarization darling, soared to $2,750 per ounce, up 15% from January, per London Bullion Market stats. China’s central bank bought 200 metric tons of gold in 2025’s first quarter alone, per World Gold Council filings.

Trade Shifts Hit Hard

De-dollarization isn’t just reserve talk—it’s trade reality. China and Brazil inked a deal in 2023 to settle trades in yuan, and by March 2025, 25% of their $150 billion annual trade skips the dollar, per Brazil’s Central Bank. Russia-China trade in yuan surged 1,500% since 2014, hitting $200 billion in 2024, per China Customs Service. BRICS nations (Brazil, Russia, India, China, South Africa) are testing a payment system to bypass SWIFT, the dollar-dominated network. A March 2025 Bloomberg report pegs its pilot transactions at $10 billion—small, but growing.

Oil, the dollar’s old ally, wavers too. Saudi Arabia now accepts yuan for 15% of its oil sales to China, up from 0% in 2020, per Saudi Aramco’s Q1 2025 earnings. That’s $20 billion annually off the dollar’s plate. “Petrodollars are fading,” warns Jim Rickards, currency expert, in a March 2025 CNBC segment. “If oil trades in yuan, the dollar’s demand drops fast.”

Stocks reflect the flux. The S&P 500 hovers at 5,900, flat year-to-date as of March 27, per NYSE data, with investors eyeing currency risks. Meanwhile, Chinese A-shares on the Shanghai Composite jumped 8% to 3,450, fueled by yuan strength, per Bloomberg. U.S. exporters like Caterpillar (CAT) took a hit—shares fell 5% to $340 since January, per Nasdaq, as tariff fears and dollar weakness bite.

Central Banks Play Defense

The Federal Reserve isn’t blind. In March 2025, Fed Chair Jerome Powell told Congress, “The dollar’s status remains robust, but we’re watching global shifts closely,” per C-SPAN transcripts. The Fed’s balance sheet holds steady at $7.5 trillion, per its March 26 release, but swap lines—dollar lifelines to allies—dropped 10% to $400 billion since 2024, per Fed data. Deutsche Bank’s March 27 report calls these lines “the dollar’s nuclear button.” If trust erodes, the fallout could accelerate.

China’s central bank, the PBOC, keeps the yuan pegged near 7 to the dollar, per March 2025 Reuters data, but its tight grip limits free float. “The yuan won’t dethrone the dollar soon—it’s not liquid enough,” says Mark Mobius, emerging markets guru, in a Bloomberg interview. Still, its use grows. Cross-border yuan payments hit $5 trillion in 2024, up 20% from 2023, per SWIFT stats.

Inflation and Your Cash

De-dollarization stings at home. A weaker dollar means pricier imports. U.S. consumer prices rose 3.2% year-over-year in February 2025, per Bureau of Labor Statistics, with imported goods like electronics up 5%. Trump’s tariff talk could push that higher—Goldman Sachs predicts 4% inflation by Q3 2025 if enacted, per its March 25 note.

Bond yields reflect nerves. The 10-year U.S. Treasury yield climbed to 4.3% by March 27, per Treasury.gov, as foreign buyers step back. That’s up from 3.8% in January. Higher yields mean costlier debt—U.S. interest payments hit $1 trillion annually, per Congressional Budget Office estimates, straining budgets.

Expert Takes: Who’s Right?

Analysts split on speed, not direction. “De-dollarization is real but gradual,” says Barry Eichengreen, UC Berkeley economist, in a March 2025 Bloomberg op-ed. He points to history: the British pound took decades to fade post-1920s. Contrast that with Rickards, who warns, “A 2025 shock—like a SWIFT rival scaling—could slash the dollar’s share 10% in a year.”

Foley at Rabobank leans cautious: “The dollar’s still 60% of forex trades—alternatives lack depth.” Yet she flags a risk: if Fed swap lines falter in a crisis, allies might ditch dollars faster. Mobius bets on gold: “Central banks hoarding bullion signal a hedge against dollar flux.”

Markets in Motion

Currency markets churn. The euro holds at $1.10, steady per ECB data, but emerging currencies like India’s rupee gained 3% to 82 per dollar since January, per Reserve Bank of India. Bitcoin, a de-dollarization wildcard, sits at $65,000, up 10% year-to-date, per Coinbase—some see it as a hedge, though volatility limits its reserve appeal.

U.S. banks brace. JPMorgan Chase (JPM) stock trades at $205, down 2% since January, per NYSE, as analysts cite dollar exposure. Its Q1 2025 earnings, due April, may show forex trading revenue shifts—last year’s $8 billion haul could shrink. Goldman Sachs (GS) at $490, up 5%, bets on global diversification, per its March 20 SEC filing.

Your Money Now: Act Smart

De-dollarization isn’t a cliff—it’s a slope. Here’s how to move:

- Diversify Holdings: The SPDR Gold Shares ETF (GLD) tracks gold at $255, up 15% in 2025, per NYSE. Add 5-10% to your portfolio—hedge inflation and dollar dips.

- Watch Emerging Markets: The iShares MSCI Emerging Markets ETF (EEM) hit $45, up 7% year-to-date, per Nasdaq. Yuan strength lifts it—consider a 5% stake.

- Lock Rates: 10-year Treasuries yield 4.3%. Buy now if you need bonds—yields may rise, dropping prices.

- Cut Debt: Credit card rates near 20%, per Fed data. Pay down fast—dollar flux could hike borrowing costs.

- Stay Liquid: Keep 3-6 months’ cash in high-yield savings at 4.5%, per FDIC averages. Flexibility beats panic.

The Long Game

No one’s burying the dollar yet. It’s 57% of reserves, 60% of trades, and the Fed’s still the world’s lender of last resort. But the trend’s clear: reliance is fraying. China’s gold buys, BRICS payment tests, and Saudi’s yuan shift aren’t bluffs—they’re moves. The IMF projects the dollar’s reserve share could dip to 50% by 2030 if trends hold.

For now, markets adapt. U.S. GDP growth holds at 2.5% for Q1 2025, per Commerce Department estimates, but import costs nibble profits. Companies like Walmart (WMT), at $75 per share, up 3%, per NYSE, tweak supply chains—its Q1 earnings showed a 2% cost rise from dollar weakness.

Stay sharp with Ongoing Now 24—de-dollarization’s slow burn could spark fast money shifts.